We’ve all been there. You file your income tax return with confidence, hit submit, and then realize three weeks later—you forgot to report that freelance income, or you missed claiming a deduction that could have saved you thousands. Panic sets in. Will the tax department notice? Am I looking at penalties? Will this affect my loan application?

{kind=link}

Here’s the good news: the Indian tax system has your back. And as of April 2025, it has your back even more generously than before.

The Fear That Keeps Taxpayers Awake at Night

Filing income tax returns shouldn’t be stressful, yet it often is. Most salaried employees and small business owners worry about one thing above all else: making a mistake on their ITR (Income Tax Return) and facing crushing penalties.

{kind=link}

But what if I told you that the Income Tax Act provides a comprehensive safety net—a 4-year window to correct mistakes without drowning in penalties? And more importantly, the government has actually made these provisions even more taxpayer-friendly starting April 2025.

Let’s break down everything you need to know about correcting tax mistakes, the penalties involved, and the exact steps to protect yourself from unnecessary financial burden.

Understanding the New 4-Year Rule: What Changed in 2026?

The Finance Act 2025 brought significant changes to how taxpayers can amend their returns. The biggest news? The deadline to file an updated return has been extended from 24 months (2 years) to 48 months (4 years) from the end of the relevant assessment year.

For example, if you filed your return for FY 2024-25 (assessed in AY 2025-26), you now have until March 31, 2030 to correct any errors or report missed income. That’s four full years to get things right.

Why does this matter? Because life happens. You might discover additional income sources, find receipts for missed deductions, or realize your tax preparer made an error. Instead of rushing to fix things within two years, you now have breathing room.

Three Ways to Fix Your Tax Mistakes (And Their Deadlines)

Not all tax corrections are created equal. Depending on when you discover the error, you have three different paths forward. Understanding which one applies to your situation can save you substantial penalty amounts.

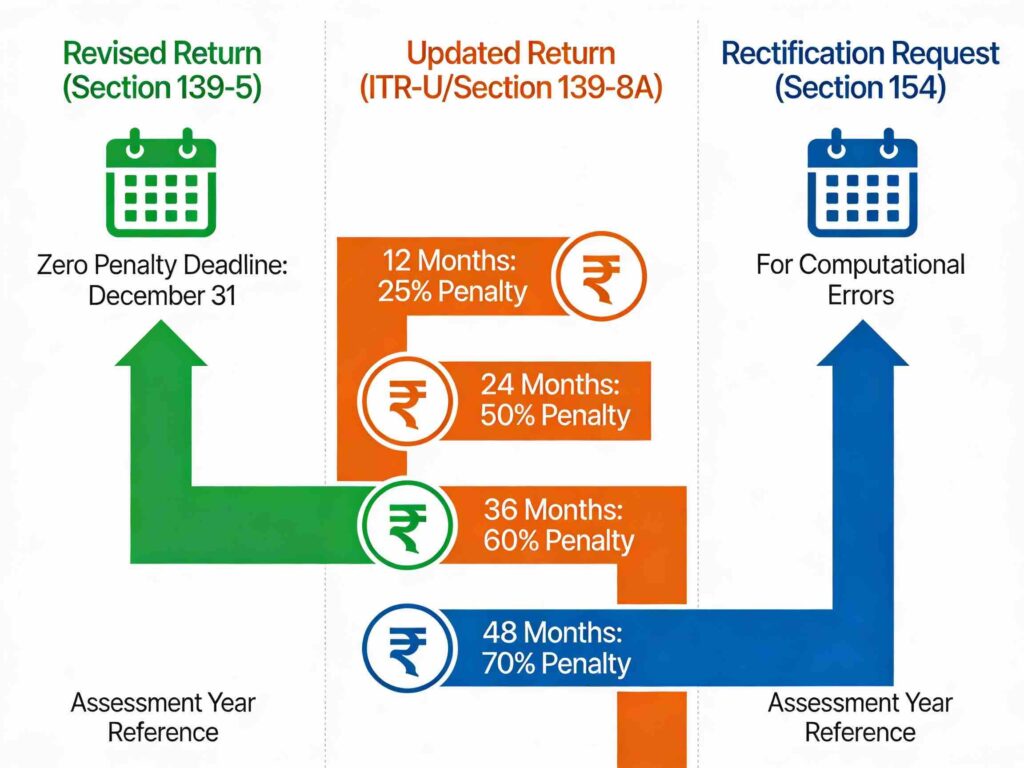

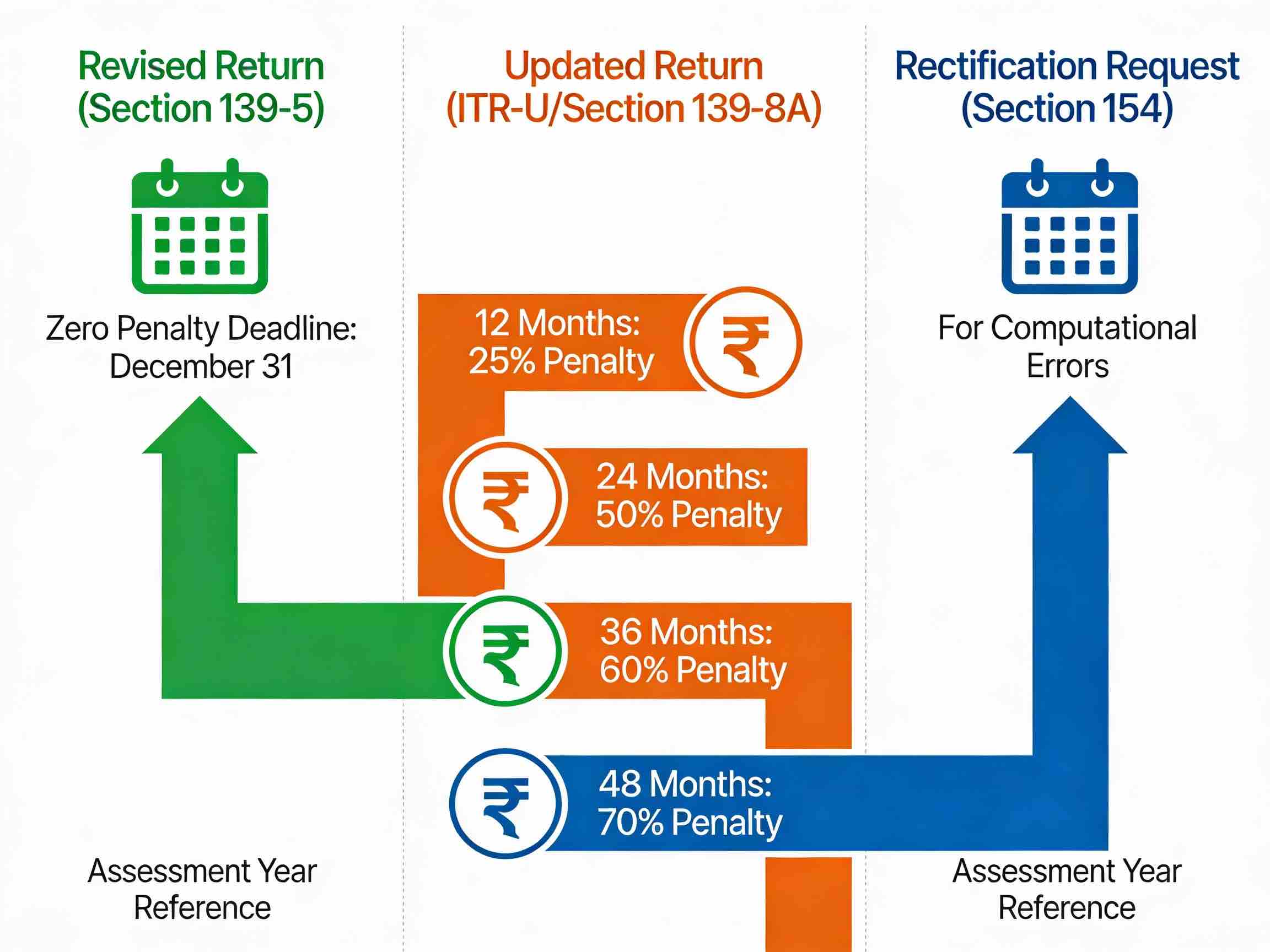

1. The Revised Return: The Penalty-Free Option (Section 139(5))

This is the gold standard for tax corrections—no additional penalties, no extra interest, no drama.

When you can use it: Before December 31 of the assessment year, or before the tax department completes the assessment process, whichever comes first.

What it costs: Nothing. Zero additional tax, zero penalties.

How many times: You can file as many revised returns as you need within the deadline.

Perfect for: Errors discovered quickly after filing—maybe you realized you forgot to report interest income from your savings account, or you want to claim an additional deduction before the year closes.

Real example: You filed your ITR on September 15, and on November 20, you discover you missed reporting ₹50,000 in freelance income. You have until December 31 to file a revised return. No penalty. Problem solved.

2. The Updated Return (ITR-U): Your Second Chance with a Price (Section 139(8A))

This is the workhorse provision—it catches all the mistakes that slip through the revised return deadline. It’s your safety net when you’ve missed the convenient window, but you want to come clean voluntarily.

When you can file: Within 4 years from the end of the assessment year (just extended from 2 years as of April 2025).

What it costs: Additional tax ranging from 25% to 70%, depending on how late you file.

Here’s the penalty breakdown that keeps many accountants up at night:

| Filing Timeline | Additional Tax on Top of Original Tax & Interest |

|---|---|

| Within 12 months from AY end | 25% |

| Within 24 months from AY end | 50% |

| Within 36 months from AY end | 60% |

| Within 48 months from AY end | 70% |

How many times: Only once per assessment year. You can’t keep tweaking your return endlessly.

Perfect for: Discovering missed income after the revised return deadline has passed, reporting unreported income voluntarily, or correcting deductions you forgot about.

Important limitation: You cannot use ITR-U to claim additional refunds or report losses. It’s specifically for reporting additional tax liability.

The math example: Let’s say you owed ₹1,00,000 in original tax but forgot to report ₹2,00,000 in income. If you file the updated return within 12 months, you’ll owe the additional tax on that ₹2,00,000 PLUS 25% penalty. File in the 4th year, and that penalty jumps to 70%.

3. The Rectification Request: For Computational Errors (Section 154)

Sometimes the mistake isn’t conceptual—it’s computational. Your TDS (Tax Deducted at Source) claim is wrong, you mistakenly added numbers incorrectly, or your challan details got jumbled.

When to use it: When you or the tax department discovers computational errors.

Cost: Minimal—only for correcting the actual error, no additional penalties.

How to file: Log into your e-filing portal, select “Rectification Request,” provide details of the error, and submit.

Best for: TDS mismatches, incorrect challan numbers, mathematical errors in calculations.

Common Tax Mistakes People Make (And Then Panic About)

Let me paint you a realistic picture of the most frequent errors that trigger the “Oh no, I need to file a corrected return” moment:

Unreported income sources:

- Freelance earnings from side gigs

- Interest from savings accounts or fixed deposits

- Rental income from a property

- Capital gains from stock sales

- Income from online platforms (YouTube, blogging, etc.)

Missed deductions:

- ₹1.5 lakh annual investment in PPF, ELSS, or life insurance (Section 80C)

- HRA (House Rent Allowance) claims without proper documentation

- Education loan interest (Section 80E)

- Home loan interest (Section 24)

- Investment in NPS (Section 80CCC)

TDS-related issues:

- TDS credited in the wrong financial year

- Form 26AS showing mismatches

- Duplicate TDS entries from employers

Form selection errors:

- Filing ITR-2 when you should have filed ITR-1

- Choosing the wrong category for self-employment income

How to Know If You REALLY Need to File a Corrected Return

Here’s a practical question: does every small error require correction? Not necessarily. The tax department uses data matching extensively, but smaller amounts sometimes slip through if the effort to track them doesn’t justify the administrative cost.

However, you SHOULD definitely correct if:

- You completely forgot to report a significant income source

- You’re aware of the error and fear discovery (it’s better to come forward voluntarily)

- Your Form 26AS shows TDS that wasn’t claimed in your original return

- The error affects your eligibility for loans or credit (banks often cross-check ITR accuracy)

- You’re claiming deductions or exemptions that require you to show corresponding income

You can probably overlook if:

- The error is ₹5,000 or less (unlikely to trigger notice)

- It’s a one-time clerical mistake in a minor figure

- You’ve already paid the full tax liability (even if income was misreported)

Reality check: Voluntary disclosure is always safer. The penalties for being caught are far steeper than the penalties for correcting mistakes voluntarily.

The Step-by-Step Process: How to Actually File a Corrected Return

Let’s make this practical. Here’s exactly what to do when you realize you’ve made a mistake:

Step 1: Identify the error and the deadline that applies

- Did you discover it before December 31? File a revised return (zero penalty).

- Is it after December 31 but within 4 years? File an updated return (ITR-U, with penalty).

Step 2: Gather all documentation

- Original ITR filed

- Proof of the missed/incorrect income (bank statements, Form 16, certificate of investment, etc.)

- Evidence of tax payment (challan copies, Form 26AS)

- Any communications from the tax department (if relevant)

Step 3: Calculate the additional tax liability

- Determine the additional taxable income

- Apply the applicable tax rate for your income bracket

- Calculate interest (if applicable)

- Add the penalty amount if filing an updated return

Step 4: File the corrected return

- Log into the e-filing portal (incometaxindiaefiling.gov.in)

- Select “File Return” → Choose the relevant ITR form → Select “Revised Return” (if within deadline) or “Updated Return” (if after deadline)

- Fill in the corrected information

- E-verify the return (via OTP, EVC, or Aadhaar OTP)

- Submit

Step 5: Make the payment

- If you owe additional tax, pay it immediately via challan (Form 16A)

- Paying before filing strengthens your case for penalty abatement if you ever face scrutiny

- Maintain proof of payment with your records

But What About Penalties? Can I Avoid Them?

This is the question everyone asks. And yes, there are ways to minimize or even eliminate penalties:

Penalty Abatement: The First-Time Relief Option

Many taxpayers don’t realize that if you’ve filed returns on time for the past three years and this is your first penalty, you can request first-time penalty abatement. It’s a one-time relief that can wipe out the entire penalty if approved.

To request abatement:

- File your corrected return with a detailed explanation letter

- Explicitly mention “penalty abatement request”

- Explain the circumstances that led to the error (overlooked income, lack of documentation, confusion about reporting requirements, etc.)

- Show good faith (you’re coming forward voluntarily, not after being caught)

The tax department often grants this relief for honest taxpayers making genuine mistakes.

Reasonable Cause Relief

If circumstances beyond your control caused the error—medical emergency, loss of documents in a fire, reliance on incorrect advice from a professional—you might qualify for reasonable cause relief. You’ll need documentation supporting your claim, but it’s worth exploring.

Let’s Talk About Fear (The Actual Psychology Here)

Here’s what I’ve observed in speaking with countless taxpayers: the fear of filing a corrected return is usually worse than the actual correction itself.

You imagine:

- The tax department coming after you with notices

- Your loan application being rejected

- Massive penalties eating your savings

- Criminal prosecution

The reality is usually much simpler:

- You file a corrected return quietly through the portal

- If it’s within the deadline and penalty-free, nothing happens

- If it’s with a penalty, you pay it and move on

- The tax department simply processes the correction

The worst-case scenario is far less catastrophic than the fear suggests. And the best case—that you voluntarily correct before anyone notices—is far more common.

The psychological shift: Stop thinking of correction as “admitting guilt.” Think of it as “housekeeping.” You’re updating your records because that’s what responsible taxpayers do.

Real-World Scenarios: How This Applies to Your Situation

Scenario 1: The Salaried Employee Who Forgot Freelance Income

Priya filed her ITR for AY 2025-26 in August, reporting ₹8 lakh salary income. Three months later, she realized she’d earned ₹3 lakh from freelance content writing that she didn’t report.

- Discovery date: November 2025

- Applicable option: Revised return (Section 139(5))

- Deadline: December 31, 2025

- Penalty: Zero

- Action: File revised return including the ₹3 lakh freelance income, pay the additional tax, verify, and submit

Scenario 2: The Self-Employed Professional Who Missed a Deduction

Raj filed his ITR and claimed ₹80,000 under Section 80C. Six months later, his CA reminds him he invested ₹2 lakh in an NPS account that could also be claimed.

- Discovery date: January 2026

- Applicable option: Updated return (ITR-U, Section 139(8A))

- Deadline: March 31, 2029 (48 months from AY end)

- Penalty: 50% of additional tax saved (since he’s filing within 24 months)

- Action: File ITR-U with the additional ₹1.2 lakh deduction claim, calculate the tax benefit, pay 50% penalty on the tax saved, and submit

Scenario 3: The Investor Who Overlooked Capital Gains

Meera sold mutual fund units in March 2025, realizing a long-term capital gain of ₹50,000. She completely forgot to report it on her ITR filed in July 2025.

- Discovery date: September 2025

- Applicable option: Revised return (Section 139(5))

- Deadline: December 31, 2025

- Penalty: Zero

- Action: File revised return including the capital gains, pay the additional tax on the gains (depending on her tax bracket), verify, and submit

Your Action Plan: What to Do Right Now

If you suspect you’ve made an error on your return:

- Don’t panic. The system is designed to accommodate corrections.

- Act quickly. Whether you qualify for zero penalty (revised return) or additional penalty (updated return), sooner is always better than later.

- Gather documentation. Proof of income, investment receipts, Form 16s, and bank statements.

- Consult if unsure. A CA or tax professional can calculate the exact tax impact and ensure everything is filed correctly.

- Pay upfront. If you owe additional tax, paying it before or with the corrected return filing looks better than paying after a notice.

- Keep records. Maintain copies of your corrected return filing, payments, and all supporting documents for at least 8 years.

The Bottom Line: Mistakes Are Forgivable, Silence Isn’t

The Indian tax system has evolved significantly in recent years. The government recognizes that honest taxpayers sometimes make honest mistakes, and it’s providing multiple pathways to correct them—including a newly extended 4-year window.

What the tax department doesn’t forgive as easily is silence. Deliberately hiding income or knowingly misreporting is a different beast entirely. But correcting unintentional errors? That’s not just forgiven; it’s encouraged through penalties that decrease if you come forward voluntarily.

The 4-year return filing window, the revised return option with zero penalties, and the updated return facility with progressive penalties—these are all safeguards designed to protect you. Use them.

Your tax return should reflect your actual financial situation. If it doesn’t, the time to fix it is now—not when the tax department calls you in for scrutiny, and definitely not when you’re applying for a loan and your ITR doesn’t match your bank statements.

Stop worrying about tax mistakes. Start correcting them. Your peace of mind is worth far more than the penalties you’re imagining.

Disclaimer: This article provides general guidance on Indian income tax rules as of 2026. Tax situations are individual and complex. Always consult with a qualified Chartered Accountant or tax professional for specific advice applicable to your circumstances. The information provided is based on current tax laws and may change with future amendments.

Have you faced a situation where you needed to correct your tax return? Share your experience in the comments below—anonymously, of course!

- Is Your Online MBA Tax-Deductible? The 2026 Blueprint to Upskill and Save Lakhs on Interest

Pursuing an online MBA? Discover how working professionals can claim unlimited tax benefits on education loan interest under Section 80E. Learn the eligibility rules, calculation methods, and smart ways to maximize your tax savings while upgrading your career.

Pursuing an online MBA? Discover how working professionals can claim unlimited tax benefits on education loan interest under Section 80E. Learn the eligibility rules, calculation methods, and smart ways to maximize your tax savings while upgrading your career. - Budget 2026 Predictions: Top 5 Expectations Likely to Become Reality

Budget 2026 is around the corner! Discover our top 5 predictions—like tax relief hikes and railway boosts—that are most likely to happen. Get ahead with smart insights for your finances.

Budget 2026 is around the corner! Discover our top 5 predictions—like tax relief hikes and railway boosts—that are most likely to happen. Get ahead with smart insights for your finances. - Budget 2026: Why Your Marriage Certificate Could Be Your Biggest Tax-Saving Tool This Year

Budget 2026 eyes joint taxation for couples—pool incomes, slash taxes by 20-30%! Save lakhs with optional filing. Explore how it beats income tax slabs, boosts tax savings, and what it means for your family finances. Will FM approve? Read now!

Budget 2026 eyes joint taxation for couples—pool incomes, slash taxes by 20-30%! Save lakhs with optional filing. Explore how it beats income tax slabs, boosts tax savings, and what it means for your family finances. Will FM approve? Read now! - Sunita Williams’ Secret: Astronaut Mindset That Builds Crores via SIP Investing

Discover Sunita Williams’ astronaut mindset for wealth building: Solve crises “one bite at a time” like mutual fund SIP investing. Learn disciplined saving, risk pivots, and best mutual funds India strategies from her 27-year NASA career.

Discover Sunita Williams’ astronaut mindset for wealth building: Solve crises “one bite at a time” like mutual fund SIP investing. Learn disciplined saving, risk pivots, and best mutual funds India strategies from her 27-year NASA career. - HDFC Bank Q3 Surprise: Profit Jumps 11.5% – Why Experts Call It a ‘Screaming Buy’ at ₹930

HDFC Bank’s Q3 FY26 results shine: 11.5% profit surge to ₹18,653 Cr, GNPA at 1.24%, deposits up 11.5%. Beats estimates amid deposit wars—strong buy for 2026? Stock eyes ₹1,000 breakout.

HDFC Bank’s Q3 FY26 results shine: 11.5% profit surge to ₹18,653 Cr, GNPA at 1.24%, deposits up 11.5%. Beats estimates amid deposit wars—strong buy for 2026? Stock eyes ₹1,000 breakout. - Withdraw PF Money in Seconds? EPFO’s New UPI Update is the Game-Changer

Discover EPFO UPI withdrawal: Instant PF access in minutes via PhonePe or Google Pay. Step-by-step guide, eligibility, benefits, and tax rules for 2026. Skip delays—empower your savings today!

Discover EPFO UPI withdrawal: Instant PF access in minutes via PhonePe or Google Pay. Step-by-step guide, eligibility, benefits, and tax rules for 2026. Skip delays—empower your savings today! - The Truth Behind the “TCS Employee Salary Drop”: Viral News, Variable Pay and What It Means for You

Discover the real reasons behind the viral TCS employee salary drop. From variable pay cuts to strict WFO mandates and performance bands, learn why IT take-home pay is shrinking and how to protect your earnings effectively.

Discover the real reasons behind the viral TCS employee salary drop. From variable pay cuts to strict WFO mandates and performance bands, learn why IT take-home pay is shrinking and how to protect your earnings effectively. - This One No-Shop Weekend Hack Could Save You ₹50,000 Yearly—Here’s How

Discover how one no-shop weekend monthly saves ₹50,000 yearly. Learn proven strategies to overcome impulse buying, build financial discipline, and transform weekend spending habits with our actionable no-spend challenge guide.

Discover how one no-shop weekend monthly saves ₹50,000 yearly. Learn proven strategies to overcome impulse buying, build financial discipline, and transform weekend spending habits with our actionable no-spend challenge guide. - The ₹1 Magic: Transform Pocket Change Into ₹1,378 With This Simple 52-Week Plan

Transform your finances with India’s most popular 52-week money challenge. Save just ₹1 in week one, building to ₹52 by year-end for a total of ₹1,378. Discover the reverse challenge, practical tips, and how consistent saving habits create lasting financial freedom.

Transform your finances with India’s most popular 52-week money challenge. Save just ₹1 in week one, building to ₹52 by year-end for a total of ₹1,378. Discover the reverse challenge, practical tips, and how consistent saving habits create lasting financial freedom. - Stop! Don’t “Liquidate” Your ₹500 Notes Yet: What the New RBI Circular Actually Says

GOI debunks viral ₹500 note discontinuation rumor. Fake news claimed RBI would ban notes by March 2026. Official clarification: ₹500 notes remain legal tender, ATMs continue dispensing them. Learn how to spot fake currency news and verify financial information.

GOI debunks viral ₹500 note discontinuation rumor. Fake news claimed RBI would ban notes by March 2026. Official clarification: ₹500 notes remain legal tender, ATMs continue dispensing them. Learn how to spot fake currency news and verify financial information.